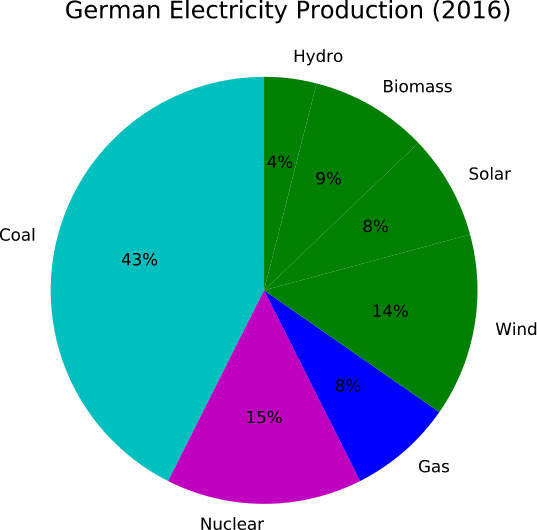

Germany’s electricity portfolio

In our last posts we introduced electrical energy storage (EES) and the EU market for EES. Now, we focus on some important EU members, beginning with Germany. The country’s electrical energy portfolio reflects its status among the most progressive countries in the world in terms of climate action. As of November 2016, Germany had produced ~35% of its 2016 electricity needs from renewable sources as outlined in the Figure below.

The growth of renewable energy has been driven by Germany’s strong energy transition policy – the “Energiewende” – a long-term plan to decarbonize the energy sector. The policy was enacted in late 2010 with ambitious GHG reduction and renewable energy targets for 2050 (80-95% reduction on 1990 GHG levels and 80% renewable-based electricity).

A major part of the 2010 Energiewende policy was the reliance on Germany’s 17 nuclear power plants as a “shoulder fuel” to help facilitate the transition from fossil fuels to renewables. In light of the Fukushima disaster just six months after the enactment of the Energiewende, the German government amended the policy to include an aggressive phase-out of nuclear by 2022 while maintaining the 2050 targets. This has only magnified the importance of clean, reliable electricity from alternative sources like wind and solar.

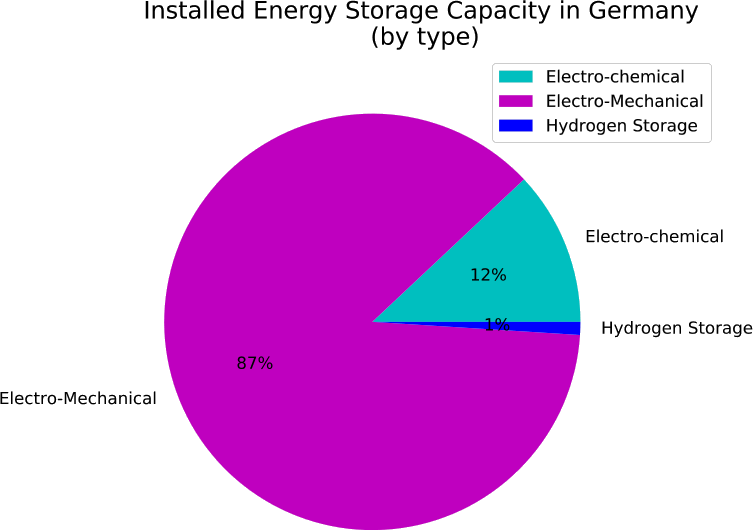

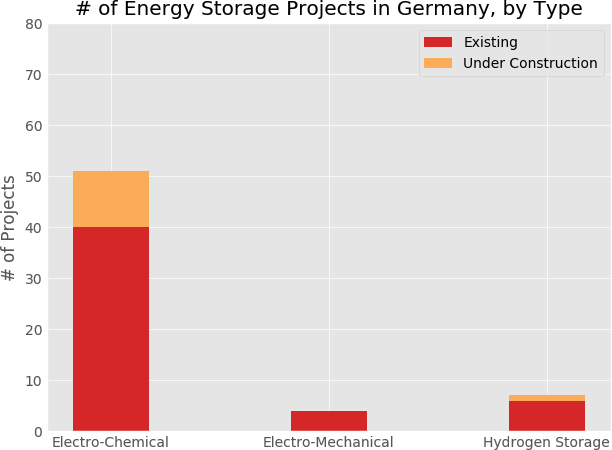

Existing Energy Storage Facilities

As of late 2016, there is 1,050 MW of installed (non-PHS) energy storage capacity in Germany. The majority of this capacity is made up of electro-mechanical technologies such as flywheels and compressed air energy storage (CAES; see figure below).

However, these numbers are somewhat skewed based on the fact that the electro-mechanical category is essentially two large capacity CAES plants. In reality, electro-chemical projects (mainly batteries) are much more prevalent and represent the vast majority of growth in the German storage market. There are currently 11 electro-chemical type energy storage projects under development in Germany and no electro-mechanical projects under development (see figure below).

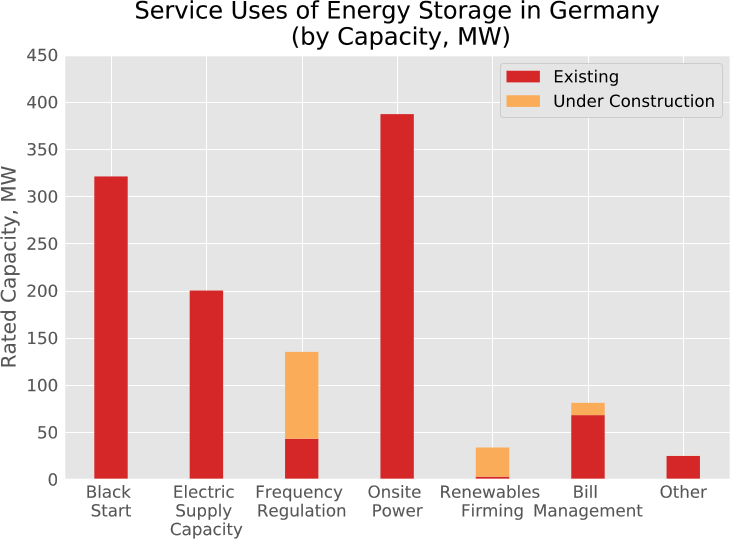

Services Uses of Energy Storage

As outlined earlier, there are a multitude of service uses for EES technologies. Currently the existing EES fleet in Germany serves grid operations and stability applications (black start, electric supply capacity), and on-site power for critical transmission infrastructure. A breakdown of service uses in the German market is shown below.

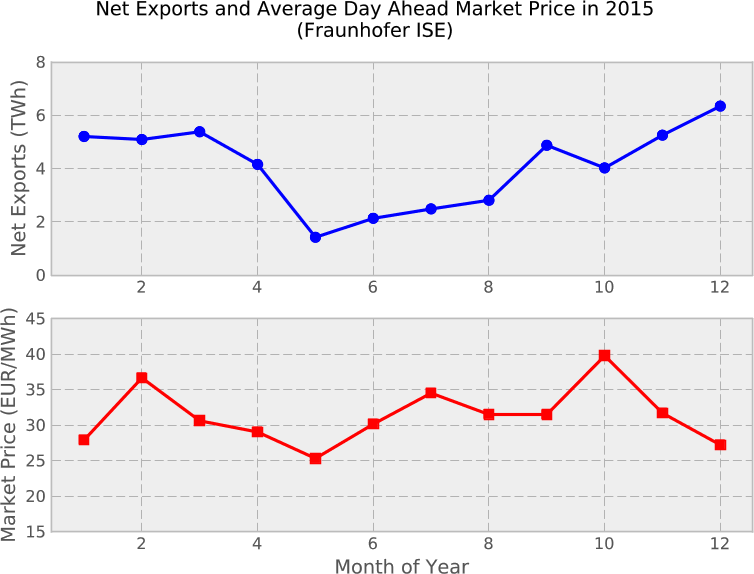

Most notable in is the fact that renewables capacity firming only represents 0.3% of EES currently operating in Germany, excluding pumped hydro storage. In order to understand this, it must be noted that Germany is a net exporter of electricity (next figure below). Having one of the most reliable electrical grids in the world and an ideal geographical location give Germany excellent interconnection to a variety of neighboring power markets; making it easy to export any excess electricity.

This “export balancing” is a primary reason why the EES market has not seen similar growth as renewable energy in Germany − it is easy for Germany to export power to balance the system load during periods of peak renewable production. However, there are negative aspects of this energy exporting such as severe overloading of transmission infrastructure in neighboring countries.

Energy Storage Market Outlook

Logic seems to indicate that with aggressive renewable energy targets, a nuclear phase-out, and increased emphasis on energy independence Germany will need to develop more EES capacity. However, many have conjectured that the lagging expansion of EES in the short and medium term will not pose a barrier to the Energiewende. In fact, some claim that EES will not be a necessity in the next 10-20 years. For example, even when Germany reaches its 2020 wind and solar targets (46 GW and 52 GW, respectively), these would generally not exceed 55 GW of supply and nearly all of this power will be consumed domestically in real-time. Thus, no significant support from EES would be required.

The German Institute for Economy Research echos these sentiments and argue that the grid flexibility needed with significant renewable energy capacity could be provided by more cost-effective options like flexible base-load power plants and better demand side management. Additionally, innovations in power-to-heat technologies which would use surplus wind and solar electricity to feed district heating systems present significant opportunity, while creating a new market of energy service companies.

Power-to-Gas

Germany’s Federal Ministry of Transport and Digital Infrastructure found that P2G is ideally suited for turning excess renewable energy into a diverse product that can be stored for long periods of time and Germany has been the central point for P2G technology development in recent years. There are currently seven P2G projects either operating or under construction in Germany.

While there is work being done, economically feasible production of P2G is currently not achievable due to limited excess electricity and low guaranteed capacity. This limited excess electricity, is an example of the effect of power exports discussed earlier. While there may not be a significant commercial market in the short-term, introduction of P2G for transport could act as an additional driver behind continued renewable energy development in Germany.

In our next post, we cover the energy storage market of the United Kingdom.

(Jon Martin, 2019)