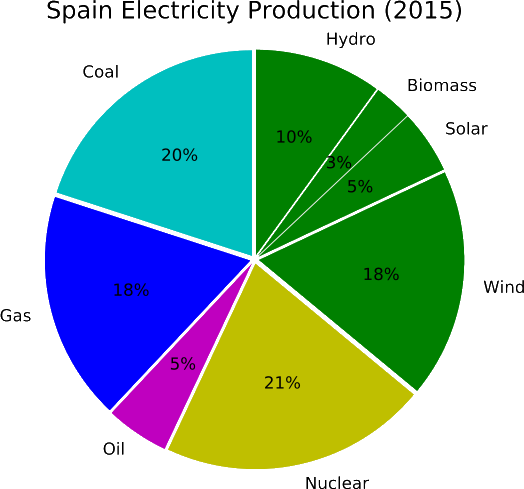

Electricity Production in Spain (Source: International Energy Agency, 2015)

While fuel oil is still used for electricity in Spain, it should be noted that this is exclusive to the non-peninsular areas of Spain (i.e. Canary Islands, Balearic Islands, Cueta, Melilla, and several other small islands).

By 2020, 20% of Spain’s final energy consumption must come from renewable energy sources – as mandated in the 2009 EU Directive 28. However, Spain will likely miss this target. In the early 2000’s Spain was a global leader in renewable energy. For example, in 2005 Spain became the first country to mandate PV installations on all new buildings and ranked 5th globally in total renewable energy investments. However the renewable energy industry has stagnated significantly over the past decade. Unfortunately, Spain, which drove the global market in 2008, has virtually disappeared from the PV picture due to retroactive policy changes and new tax on self-consumption.

The policy changes and self-consumption taxes allude to the Royal Decree 900/2015 on self-consumption, a law enacted by the Spanish government in October 2015, which aims to financially penalize the self-consumption of electricity. Under the new law solar PV producers (residential PV owners, for example) are required to not only pay a tax on the energy they self-consume, but also must pay the same transmission & distribution fees they would have paid on an equivalent amount of electricity purchased from the grid. In addition to these charges and taxes, owners of systems 100 kW and smaller – most residential system owners – are prohibited from selling excess electricity from the grid. Instead, they must give it to the grid for free. Furthermore, this law is retroactive; meaning existing PV systems must comply or face a penalty. Penalties under the self-consumption law range from as low as EUR 6-million up to a maximum of EUR 60-million – about twice the fine for leaking radioactive waste. The Spanish government see’s self-consumption as a risk to tax revenues at the current high electricity prices.

Spain is still the world leader in concentrated solar power capacity (2.5 MW). However, no new plants were constructed since and there are currently no new plants under construction or in planning.

Energy Storage Market Outlook – Spain

Although initial drafts of the “self-consumption” law had strict provisions against battery storage systems, the final version does permit energy storage systems – although under conditions that make them impractical. While owners of solar-plus-storage systems are subject to additional charges, they also cannot reduce the amount of power that they have under contract from their utility company.

At this point in time, it appears as if the self-consumption law has effectively halted any investment in renewable energy and/or energy storage projects in Spain.

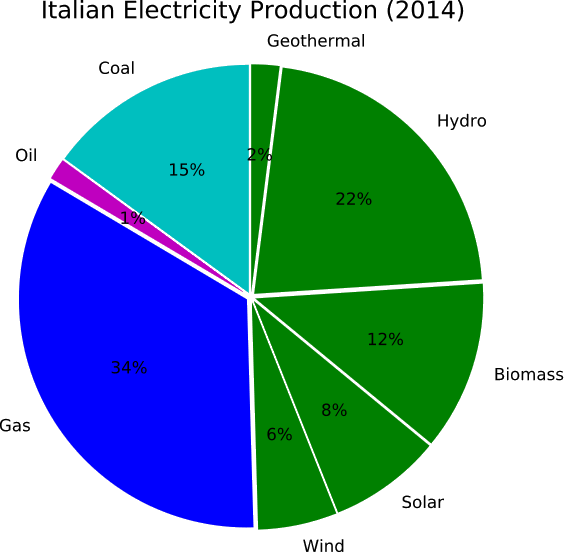

In our previous post we briefed you on the energy storage potential in the United Kingdom. With Brexit, Italy will become the third largest member state after Germany and France. With extensive mountain terrain in the north, Italy has long been dependent upon hydroelectric generation. Until the mid 1960s hydropower represented nearly all electricity production in Italy. The installed capacity of hydropower has been stagnant since the mid 1960s, with a rapid growth in fossil fuel based generation driving the overall share of hydropower fall from ~90% to 22% in 2014. A detailed breakdown of electricity sources in Italy is shown below.

Electricity Production in Italy (2014)

Considerable effort has been made to transition Italy to a low carbon electricity sector. As of 2016, Italy had the 5th highest installed solar capacity in the world and the 2nd highest per capita solar capacity, behind only Germany. In addition to its impressive solar progress Italy ranks 6th worldwide in geothermal with 0.9 GW.

Italy’s solar growth was propelled by feed-in-tariffs that wer enacted in 2005. This provided residential PV owners with financial compensation for energy sold to the grid. However, the feed-in-tariff program ceased on 06 July 2014 after the €6.7 billion subsidy limit was reached.

Even with its impressive accomplishments in renewable energy, traditional thermal generation (natural gas) still account for ~60% of total electricity generation in Italy. How much effort will go into reducing this number is still unclear. Italy has committed to 18% renewables by 2020 and is nearly 70% of the way there already so there is little urgency on reducing fossil-based electricity from the perspective of meeting this target. However, Italy is heavily reliant on fossil fuel imports (Deloitte) and energy security requirements will likely continue to push the development of more domestic electricity sources like renewables.

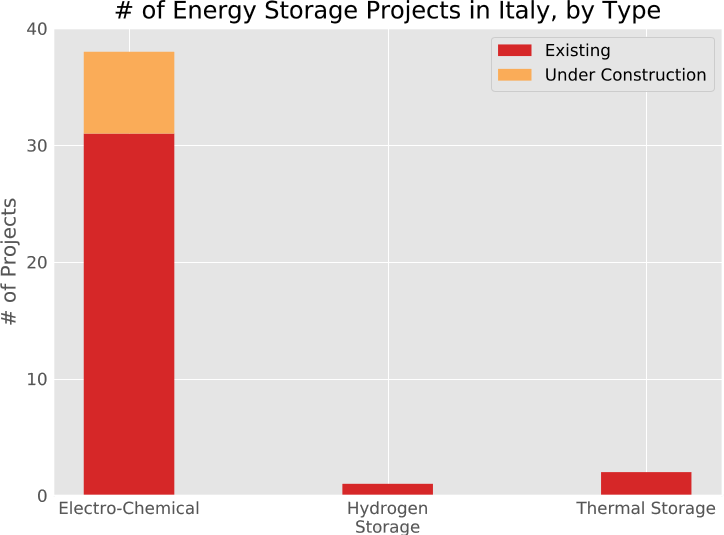

Energy Storage Facilities

Italy is dominating the electro-chemical energy storage market in Europe. With over 6,000 GWh of planned and installed electro-chemical generating capacity (~84 MW installed capacity), Italy is far ahead of 2nd place UK. This is largely due to the massive SNAC project by TERNA (Italy’s TSO), a sodium-ion battery installation totaling nearly 35 MW over three phases. A breakdown of energy storage projects, by technology type can be seen below.

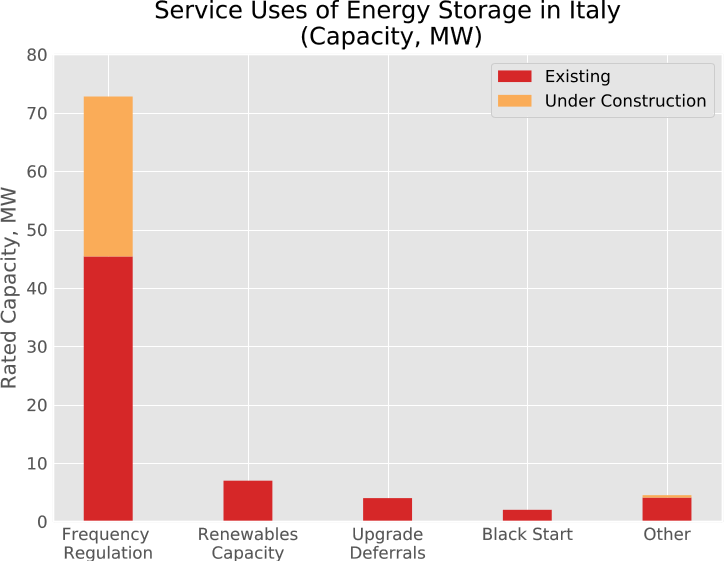

Italy is one of the top markets in the EU for energy storage and is primed for growth. The Italian TSO, TERNA, has been investigating selling energy storage as a service. In 2014 the AEEG, the electrical regulator under which TERNA operates, proposed that batteries should be treated as generation sources similar to cogeneration plants. Italy has always been a market completely dominated by a small number of big centralized utility companies and this trend is likely to continue when it comes to EES deployment. These companies have been focusing their efforts on battery technologies and are expected to continue down this path.

However, the private market could present great opportunity for P2G. The International Battery & Energy Storage Alliance have summarized the reality of Italy’s untapped energy storage market as follows: “With high solar output of 1,400 kWh/kWp, net residential electricity prices around 23 cent/kWh and currently no FIT, the Italian energy market is considered to be highly receptive for energy storage.”

Italy is now well-stocked with residential PV systems that can no longer collect subsidies. Combine this with the fact that the vast majority of homes in Italy burn natural gas imported from Russia, Libya and Algeria and it is clear that Italy presents a unique opportunity for P2G at a residential/community level. This is echoed by Energy Storage Update who in 2015 concluded that Italy was “one of the top four markets worldwide for PV-and-battery-based energy self-consumption.”

While it is unclear exactly how many residential PV systems there are in Italy, it was speculated in late 2015 that there were over 500,000 PV plants in Italy.

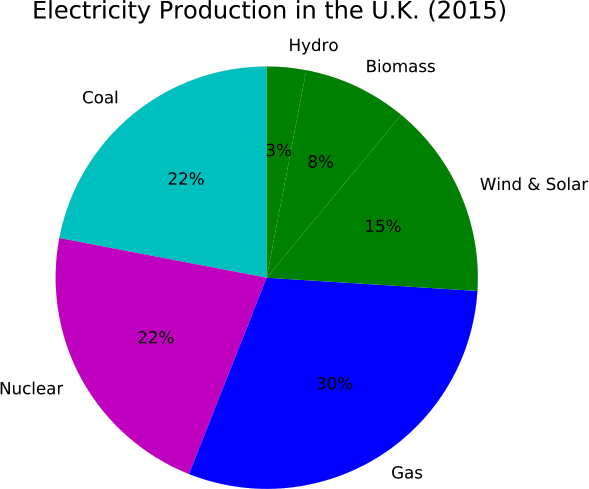

In our last post about the EU energy storage market we gave a brief overview of Germany’s situation. Now, we show how the United Kingdom prepared itself for its energy transition. Traditionally, the UK’s energy mix has been dominated by fossil fuels. This remains the status quo today, as approximately 60% of the electricity generated in the UK comes from fossil fuel sources, with another 20% coming from nuclear.

UK electricity production 2015 (Source: The UK Government)

While the UK has been heavily dependent on carbon-intensive sources of electricity, in 2008 they committed to a 15% renewable energy target (by 2020) and 80% reduction in CO2 emissions (by 2050; Department of Energy & Climate Change). However, the UK has stated that they will miss the 15% renewable target for 2020, due to the lack of properly designed policy measures. There has been considerable pressure to transition to a low carbon market and with one-quarter of existing generating capacity (mainly coal and nuclear) expected to close by 2021; it is expected that growth in renewable energy will lead to more energy storage capacities.

The UK has made excellent progress on its short-term clean energy goals and there is optimism that this trend will continue. Large-scale development of low carbon generation technologies such as wind and solar is expected to continue.

Energy Storage Facilities

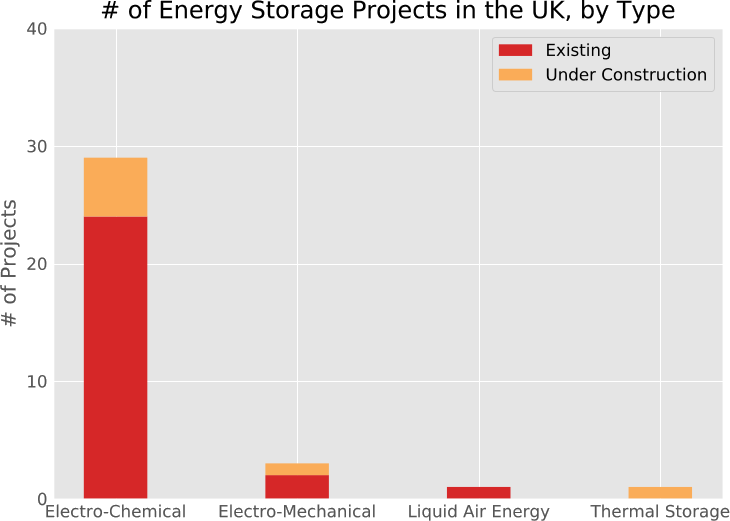

As of late 2016, there were 27 non-PHS EES plants representing 430 MW of installed capacity in the UK (Sandia National Laboratories). The UK’s energy storage portfolio is dominated by electro-chemical based technologies (primarily lead-acid and lithium-ion battery installations). This is shown below.

Number of Existing & Planned Energy Storage Facilities in the UK, by Type (Source: Sandia National Laboratories)

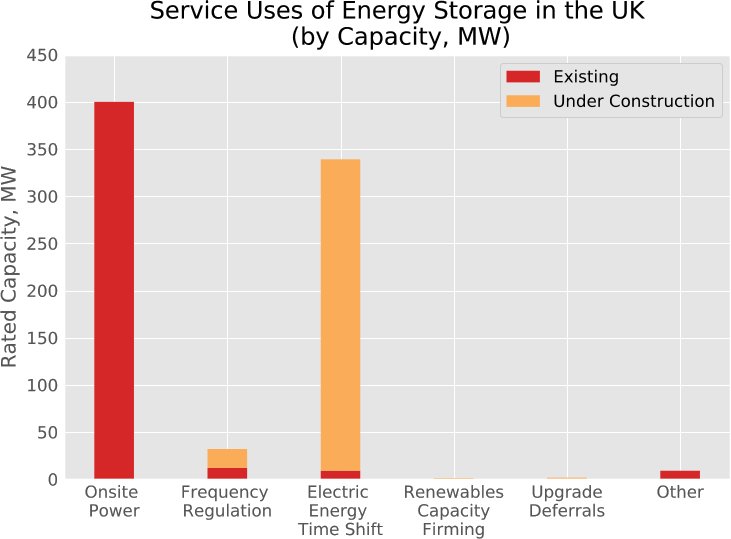

As was shown for Germany, only a very small fraction of EES facilities are dedicated to renewables capacity firming. The existing EES capacity is almost exclusively dedicated to critical transmission support (on-site power). While nearly all of the EES capacity under development is dedicated to bulk energy storage (electric energy time shift).

There is still considerable uncertainty around the growth of EES in the UK, and with such a small sample size it is difficult to infer any correlation from the data in the figure above. According to the previous UK government, however, being geographically isolated and a net importer of electricity, one would expect the UK to place a heavier focus on renewables capacity firming in the long-term.

Energy Storage Market Outlook

The UK is in the midst of a major restructuring of their electricity generating portfolio and the market under which these assets operate. With a large portion of the existing capacity due for retirement in the next 10-15 years, the UK faces challenges in meeting energy needs while balancing decarbonization efforts. As part of this, major investment is needed in all areas of the electrical grid, including energy storage.

In its Smart Power publication, the National Infrastructure Commission outlined that while the UK is being faced with challenges to cover aging infrastructure this represents an opportunity to build efficient and flexible energy infrastructure. The Commission stated that energy storage was one of the three key innovations for a “smart power revolution”.

Many other official government bodies have expressed similar thoughts regarding energy storage. In its Low carbon network infrastructure report, the Energy and Climate Change Committee stated that “storage technologies should be deployed at scale as soon as possible”, while urging the Government to eliminate the outdated and unfair regulations that have been handcuffing energy storage development in the UK (Garton and Grimwood).

In April 2016, the Government acknowledged concerns regarding the regulatory hurdles facing energy storage projects (primarily double-charging of network charges) and stated that they would begin working with the National Infrastructure Commission and ECCC to investigate the issue. While there may be regulatory hurdles hindering energy storage in the UK, the Government has shown commitment through funding. Since 2012, the government has contributed over £80 million to energy storage research. In addition to this, the Department of Energy and Climate Change have developed a new £20 million fund to help drive innovation in energy storage technologies.

Overall, the outlook for energy storage in the UK is positive. There is considerable pressure to begin developing energy storage facilities at scale from not only industry, but also many government bodies. Investors are ready as well. As stated by the National Infrastructure Commission: “businesses are already queuing up to invest”.

Simply put: regulatory hurdles are holding back growth in the UK energy storage market. With the Government making major strides in renewable energy development and being vocal about its commitment to making the UK a leader in energy storage technology, these regulatory hurdles will likely be relaxed and there should be considerable growth in the UK energy storage market in the near-term.

At this point, specific technology types and service uses have not been hypothesized in detail. However, with the UK being geographically isolated and a net importer of electricity, logic would suggest an emphasis on renewables capacity firming in the long-term to maximize domestic consumption of renewable energy. Rapidly decreasing costs in electro-chemical technologies, coupled with the fact that much of the existing gas-fired capacity will be reaching end of life by 2030 suggest that the UK EES market would not be ideal for P2G technologies.

In our last posts we introduced electrical energy storage (EES) and the EU market for EES. Now, we focus on some important EU members, beginning with Germany. The country’s electrical energy portfolio reflects its status among the most progressive countries in the world in terms of climate action. As of November 2016, Germany had produced ~35% of its 2016 electricity needs from renewable sources as outlined in the Figure below.

Electricity Production in Germany (Source: Fraunhofer ISE)

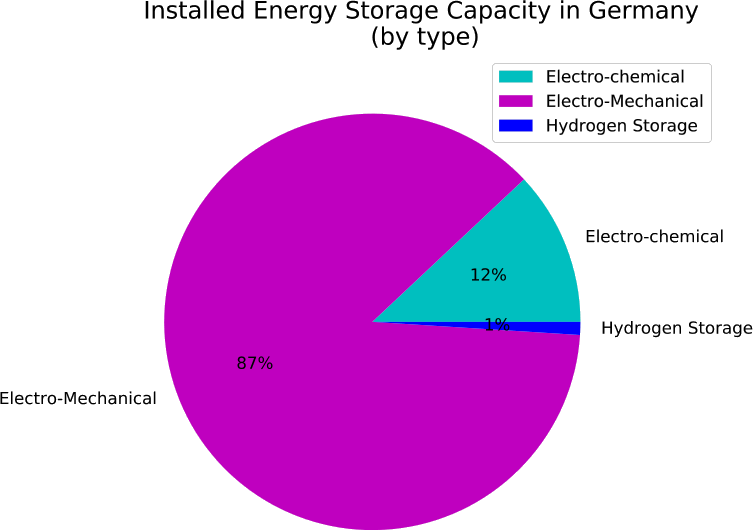

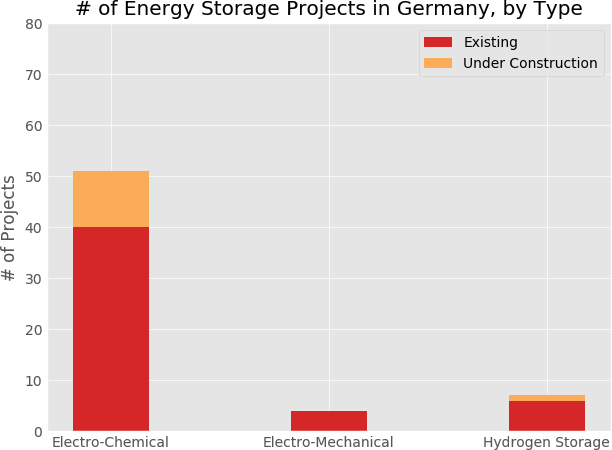

However, these numbers are somewhat skewed based on the fact that the electro-mechanical category is essentially two large capacity CAES plants. In reality, electro-chemical projects (mainly batteries) are much more prevalent and represent the vast majority of growth in the German storage market. There are currently 11 electro-chemical type energy storage projects under development in Germany and no electro-mechanical projects under development (see figure below).

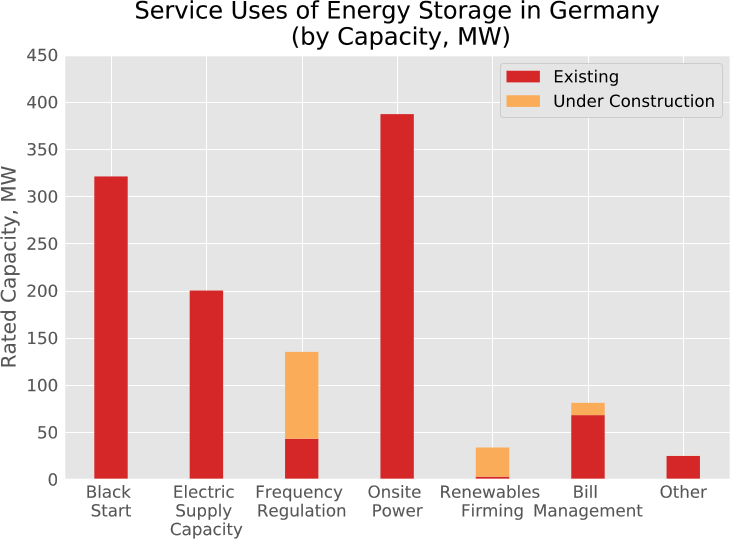

As outlined earlier, there are a multitude of service uses for EES technologies. Currently the existing EES fleet in Germany serves grid operations and stability applications (black start, electric supply capacity), and on-site power for critical transmission infrastructure. A breakdown of service uses in the German market is shown below.

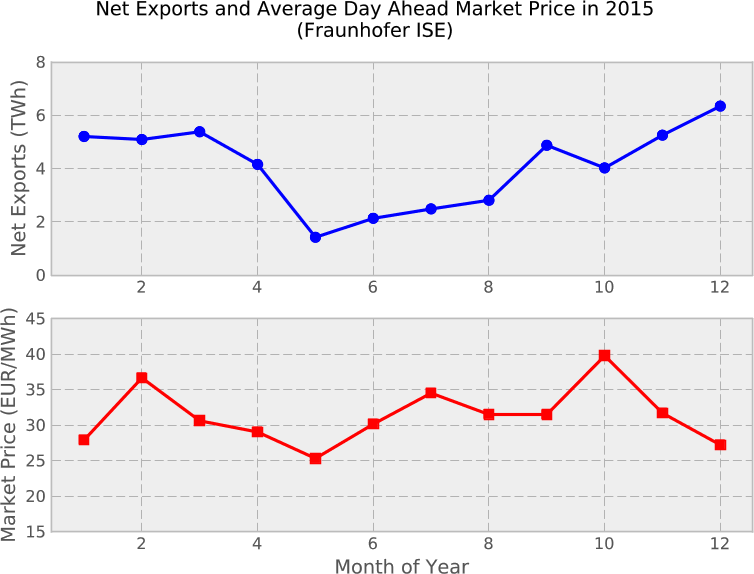

Net Exports of Electricity with Average Day-Ahead Market Pricing for Germany in 2015 (Source: Fraunhofer ISE)

Energy Storage Market Outlook

Logic seems to indicate that with aggressive renewable energy targets, a nuclear phase-out, and increased emphasis on energy independence Germany will need to develop more EES capacity. However, many have conjectured that the lagging expansion of EES in the short and medium term will not pose a barrier to the Energiewende. In fact, some claim that EES will not be a necessity in the next 10-20 years. For example, even when Germany reaches its 2020 wind and solar targets (46 GW and 52 GW, respectively), these would generally not exceed 55 GW of supply and nearly all of this power will be consumed domestically in real-time. Thus, no significant support from EES would be required.

The German Institute for Economy Research echos these sentiments and argue that the grid flexibility needed with significant renewable energy capacity could be provided by more cost-effective options like flexible base-load power plants and better demand side management. Additionally, innovations in power-to-heat technologies which would use surplus wind and solar electricity to feed district heating systems present significant opportunity, while creating a new market of energy service companies.

While there is work being done, economically feasible production of P2G is currently not achievable due to limited excess electricity and low guaranteed capacity. This limited excess electricity, is an example of the effect of power exports discussed earlier. While there may not be a significant commercial market in the short-term, introduction of P2G for transport could act as an additional driver behind continued renewable energy development in Germany.

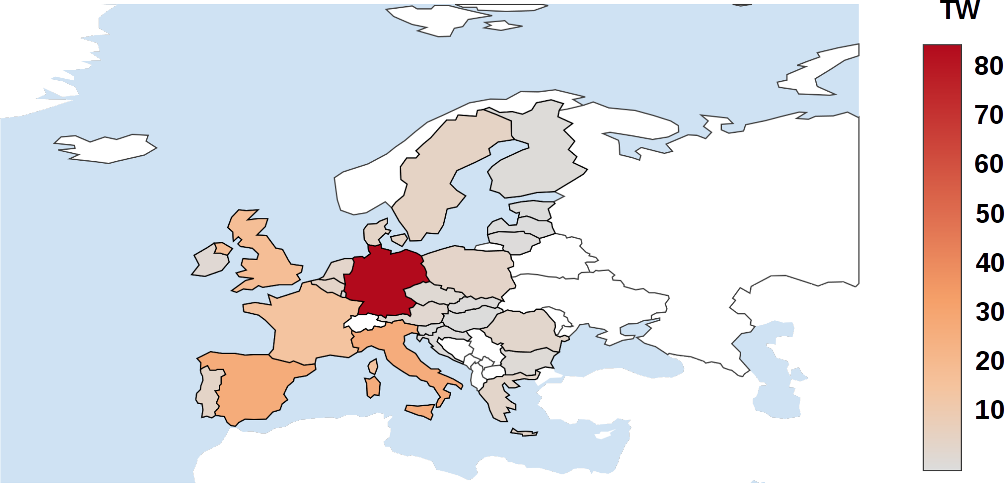

In our previous post of this blog series on Electrical Energy Storage in the EU we briefly introduced you to different technologies and their use cases. Here, we give you a short overview over the EU energy grid. Supplying approximately 2,500 TWh annually to 450 million customers across 24 countries, the synchronous interconnected system of Continental Europe (“the Grid”) is the largest interconnected power network in the world. The Grid is made up of transmission system operators (TSOs) from 24 countries stretching from Greece to the Iberic Peninsula in the south, Denmark and Poland in the north, and up to the black sea in the east. The European Network of Transmission System Operators (ENTSO-E) serves as the central agency tasked with promoting cooperation between the TSOs from the member countries in the Grid. The ENTSO-E, in essence, acts as the central TSO for Europe. With over 140 GW of installed wind and solar PV capacity, the EU trails behind only China in installed capacity. A breakdown of the individual contributions of EU member states is shown below in the figure above.

Energy Storage in the EU

For this study a number of European countries were selected for more detailed investigation into energy storage needs. These countries were selected based on a combination of existing market size, intentions for growth in non-dispatchable renewable energy and/or energy storage, and markets with a track record of innovation in the energy sector.

On a total capacity basis (installed and planned MW) the top three energy storage markets within the EU are: Italy, the UK, and Germany. These countries were selected on the basis of these existing market sizes.

Spain and Denmark were selected based on their large amounts of existing renewable energy capacity and − in the case of Denmark − the forecasted growth in renewable energy and energy storage capacity.

Each of the selected countries (Germany, UK, Italy, Spain, Denmark, Netherlands) are discussed in the proceeding sections, providing a more detailed overview outlining their current electricity portfolios and decarbonization efforts, current energy storage statistics, and a brief discussion on market outlook.

Electrical energy storage (EES) is not only a vital component in the reliable operation of modern electrical grids, but also a focal point of the global renewable energy transition. It has been often suggested that EES technologies could be the missing piece to eliminating the technical hurdles facing the implementation of intermittent renewable energy sources. In the following blog posts, selected EES markets within the European Union will be evaluated in detail.

With over 80 MW of installed wind and solar capacity, Germany is by far the leading EU nation in the renewable energy transition. However, experts have argued that Germany’s need for widespread industrial scale energy storage is unlikely to materialize in any significant quantity for up to 20-years. This is due to a number of factors. Germany’s geographic location and abundance of connections to neighbouring power grids makes exporting any electricity fluctuations relatively easy. Additionally, when Germany reaches its 2020 targets for wind and solar capacity (46 GW and 52 GW, respectively) the supply at a given time would generally not exceed 55 GW. Nearly all of this would be consumed domestically, with no/little need for storage.

When evaluating energy storage in the UK, a different story emerges. Being an isolated island nation there is considerably more focus on energy independence to go along with their low-carbon energy goals. However, the existing regulatory environment is cumbersome, and poses barriers significant enough to substantially inhibit the transition to a low-carbon energy sector – including EES. The UK government has acknowledged the existence of regulatory barriers and pledged to address them. As part of this effort, a restructuring of their power market to a capacity-based market is already underway. The outlook for EES in the UK is promising, there is considerable pressure from not only industry, but also the public and the government to continue developing EES facilities at industrial scale.

Italy, once heavily hydro-powered, has grown to rely on natural gas, coal, and oil for 50% of it’s electricity (gas representing 34% alone). The introduction of a solar FIT in 2005 lead to significant growth in the solar industry (Italy now ranks 2nd in per capita solar capacity globally) before the program ended in July 2014. In recent years there has been notable growth in electro-chemical EES capacity (~84 MW installed), primarily driven by a single large-scale project by TERNA, Italy’s transmission system operator (TSO). This capacity has made Italy the leader in EES capacity in the EU, however the market is to-date dominated by the large TSOs.

However, the combination of a reliance on imported natural gas, over 500,000 PV systems no longer collecting FIT premiums, and increasing electricity rates presents a unique market opportunity for residential power-to-gas in Italy.

Denmark is aggressively pursing a 100-percent renewable target for all sectors by 2050. While there is still no official roadmap policy on how they will get there, they have essentially narrowed it down to one of two scenario: a biomass-based scenario, or a wind + hydrogen based scenario. Under the hydrogen-based scenario there would be widespread investment to expand wind capacity and couple this capacity with hydrogen power-to-gas systems for bulk energy storage. With the Danish expertise and embodied investment in wind energy, one would expect that the future Danish energy system would be build around this strength, and hence require significant power-to-gas investment.

The renewable energy industry in Spain has completed stagnated due to retroactive policy changes and taxes on consumption of solar generated electricity introduced in 2015. The implementation of the Royal Decree 900/2015 on self-consumption has rendered PV systems unprofitable, and added additional fees and taxes for the use of EES devices. No evidence was found to suggest a market for energy storage will materialize in Spain in the near future.

The final country investigated was the Netherlands, which has been criticized by the EU for its lack of progress on renewable energy targets. With only 10% of Dutch electricity coming from renewable sources, there is currently little demand for large-scale EES. While the Netherlands may be lagging behind on renewable electricity targets, they have been a leader in EV penetration; a trend that will continue and see 1-million EVs on Dutch roads by 2025. In parallel with the EV growth, there has been a large surge in sub-100kW Li-ion installations for storing energy at electric vehicle (EV) charging stations. It is expected that these applications will continue to be the primary focus of EES in the Netherlands.

Similar to Italy, the Dutch rely heavily on natural gas for energy within their homes. This fact, coupled with an ever-increasing focus on energy independent and efficient houses could make the Netherlands a prime market for residential power-to-gas technologies.

Achieving high current densities while maintaining high energy efficiency is one of the biggest challenges in improving photoelectrochemical devices. Higher current densities accelerate the production of hydrogen and other electrochemical fuels.

Now a compact, solar-powered, hydrogen-producing device has been developed that provides the fuel at record speed. In the journal Nature Energy, the researchers around Saurabh Tembhurne describe a concept that allows capturing concentrated solar radiation (up to 474 kW/m²) by thermal integration, mass transport optimization and better electronics between the photoabsorber and the electrocatalyst.

The research group of the Swiss Federal Institute of Technology in Lausanne (EPFL) calculated the maximum increase in theoretical efficiency. Then, they experimentally verified the calculated values using a photoabsorber and an iridium-ruthenium oxide-platinum based electrocatalyst. The electrocatalyst reached a current density greater than 0.88 A/cm². The calculated conversion efficiency of solar energy into hydrogen was more than 15%. The system was stable under various conditions for more than two hours. Next, the researchers want to scale their system.

The produced hydrogen can be used in fuel cells for power generation, which is why the developed system is suitable for energy storage. The hydrogen-powered generation of electricity emits only pure water. However, the clean and fast production of hydrogen is still a challenge. In the photoelectric method, materials similar to those of solar modules were used. The electrolytes were based on water in the new system, although ammonia would also be conceivable. Sunlight reaching these materials triggers a reaction in which water is split into oxygen and hydrogen. So far, however, all photoelectric methods could not be used on an industrial scale.

2 H2O → 2 H2 + O2; ∆G°’ = +237 kJ/mol (H2)

The newly developed system absorbed more than 400 times the amount of solar energy that normally shines on a given area. The researchers used high-power lamps to provide the necessary “solar energy”. Existing solar systems concentrate solar energy to a similar degree with the help of mirrors or lenses. The waste heat is used to accelerate the reaction.

The team predicts that the test equipment, with a footprint of approximately 5 cm, can produce an estimated 47 liters of hydrogen gas in six hours of sunshine. This is the highest rate per area for such solar powered electrochemical systems. At Frontis Energy we hope to be able to test and offer this system soon.

Solar thermal systems are a good example of the particle-wave dualism expressed in Planck’s constanth: E = hf. Where h is the Planck constant, f is the frequency of the light and E is the resulting energy. Thus, the higher the frequency of the light, the higher the amount of energy. Solar thermal metal collectors transform the energy of high-frequency light by generating them to an abundance of low-frequencies through Compton shifts. Glass or ceramic coatings with high visible and UV transmittance absorb the low frequency light generated by the metal because they effectively absorb infrared light (so-called heat blockers). The efficiency of the solar thermal system improves significantly with increasing size, which is also the biggest advantage of such systems compared to photovoltaic generators. One disadvantage, however, is the downstream transformation of heat into electricity with the help of heat exchangers and turbines − a problem not only in solar thermal systems.

To provide the hot gas (supercritical CO2) to the turbines, heat exchangers are necessary. These heat exchangers transfer the heat energy generated by a power plant to the working fluid in a heat engine (usually a steam turbine) that converts the heat into mechanical energy. Then, the mechanical energy is used to generate electricity. These heat exchangers are operated at ~800 Kelvin and could be more efficient if the temperature were at >1,000 Kelvin. The entire process of converting heat into electricity is called a power cycle and is a critical process in power generation by solar thermal plants. Obviously, heat exchangers are pivotal elements in this process.

Ceramics are a great material material for heat exchanger because they can withstand extreme temperature fluctuations. However, unlike metals, ceramics are not easy to shape. Relatively coarse shapes, in turn, are made quickly and easily. In contrast, metals can be easily formed and have a high mechanical strength. Metals and ceramics have been valued for centuries for their distinctive properties. For example, bronze and iron have good impact resistance and are so malleable that they have been made into complex shapes such as weapons and locks. Ceramics, like those used to make pottery, have been formed into simpler shapes. Their resistance to heat and corrosion made ceramics a valued material. A new composite of metal and ceramic (a so-called cermet) combines these properties in amazing ways. A research group led by Mario Caccia reported now in the prestigious journal Nature about a cermet with properties that makes it usable for heat exchangers in solar thermal systems.

The history of such composites goes back to the middle of the 20th century. The advent of jet engines has created a need for materials with high resistance to heat and oxidation. On top of that, they had to deal with rapid temperature changes. Their excellent mechanical strength, which often surpassed that of existing metals, was highly appreciated by the newly created aerospace industry. Not surprisingly, the US Air Force funded more research into the production of cermets. Cermets have since been developed for multiple applications, but in most cases have been used for small parts or surfaces. The newly released composite withstands extreme temperatures, high pressures and rapid temperature changes. It could increase the efficiency of heat exchangers in solar thermal systems by 20%.

To produce the composite, the authors first produced a precursor, which was subject to further processing, comparable to potting the unfired version of a clay pot. The authors compacted tungsten carbide powder into the approximate shape of the desired article (the heat exchanger) and heated it at 1,400 °C for 2 minutes to bond the parts together. They then further processed this porous preform to produce the desired final shape.

Next, the authors heated the preform in a chemically reducing atmosphere (a mixture of 4% hydrogen in argon) at 1,100 °C. At the same temperature, they immersed the preform in a tank of liquid zirconium and copper (Zr2Cu). Finally, the preform was removed by heating to 1,350 °C. In this process, the zirconium displaces the tungsten from the tungsten carbide, producing zirconium carbide (ZrC) as well as tungsten and copper. The liquid copper is displaced from the ZrC matrix as the material solidifies. The final object consists of ~58% ZrC ceramic and ~36% tungsten metal with small amounts of tungsten carbide and copper. The beauty of the method is that the porous preform is converted into a non-porous ZrC / tungsten composite of the same dimensions. The total volume change is about 1-2%.

The elegant manufacturing process is complemented by the robustness of the final product. At 800 °C, the ZrC / tungsten cermet conducts heat 2 to 3 times better than nickel based iron alloys. Such alloys are currently used in high-temperature heat exchangers. In addition to the improved thermal conductivity, the mechanical strength of the ZrC / tungsten composite is also higher than that of nickel alloys. The mechanical properties are not affected by temperatures of up to 800 ° C, even if the material has previously been subjected to heating, e.g. for cooling cycles between room temperature and 800 °C. In contrast, iron alloys, e.g. stainless steels, and nickel alloys loose at least 80% of their strength.